Login to your Lazo One account here

Login

Do you know which early choices can cut your federal tax bill and still keep you compliant?

We write this as fellow founders who want clarity, not confusion. This Ultimate Guide gives a plain-English roadmap to federal and state obligations, key filings, and high-value elections that matter in year one.

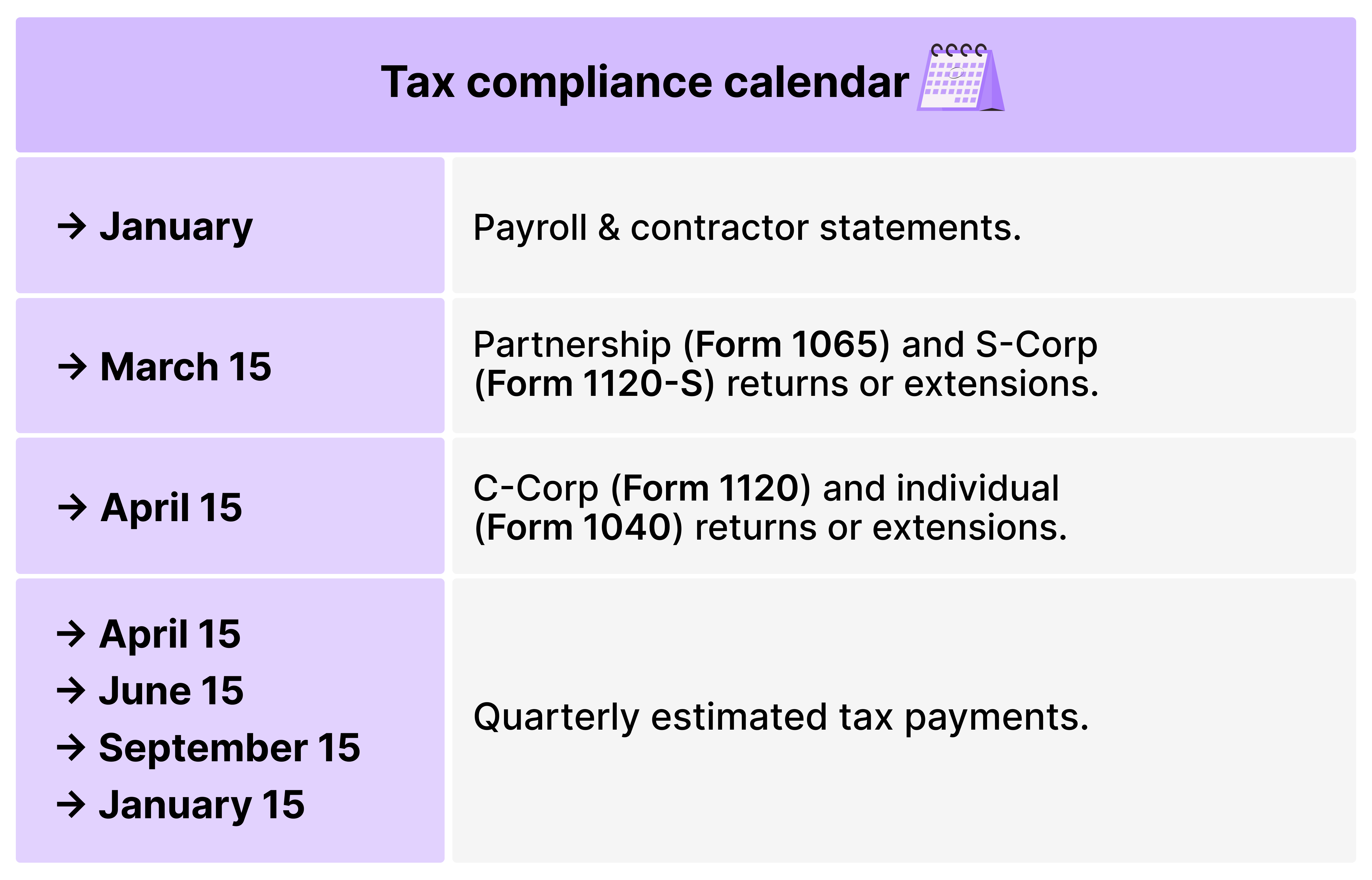

Federal corporate income for C-corps follows a flat regime and Form 1120 is required annually even with no income. Some states add a recurring minimum franchise charge and a separate corporate income tax. Key dates cluster around late January, mid-March, mid-April, and mid-quarter estimates.

We’ll walk through nexus risks, bookkeeping essentials, R&D credit opportunities, QSBS planning (note: some states do not conform), and how startup costs are capitalized and amortized. If you want help operationalizing compliance, meet Lazo.

Quick, practical clarity around filings and deadlines prevents costly surprises. Founders juggle product, hiring, and runway; missing a return deadline or quarterly estimate creates penalties and distraction.

Remote teams and LatAm–US founders face extra complexity: multiple jurisdictions can trigger filings sooner than expected (think payroll/contractor reports in late January; corporate returns or extensions by mid-March; estimates around mid-April, mid-summer, early fall, and early in the following year).

Some states layer a recurring franchise charge, their own corporate return, and nonconformity with QSBS. We focus on actions you can use today so filings stay clean and timely. For key deadlines, check 2025 US Tax Deadlines.

Get registrations right at launch. Secure an EIN immediately; it opens bank, payroll, and state accounts.

States vary widely: some impose corporate income plus franchise charges; others use gross-receipts models. Multistate revenue is apportioned by sales, payroll, and property.

Pro tips

Model after-tax outcomes at key milestones, plan QSBS early, and remember some states assess franchise charges even with little activity.

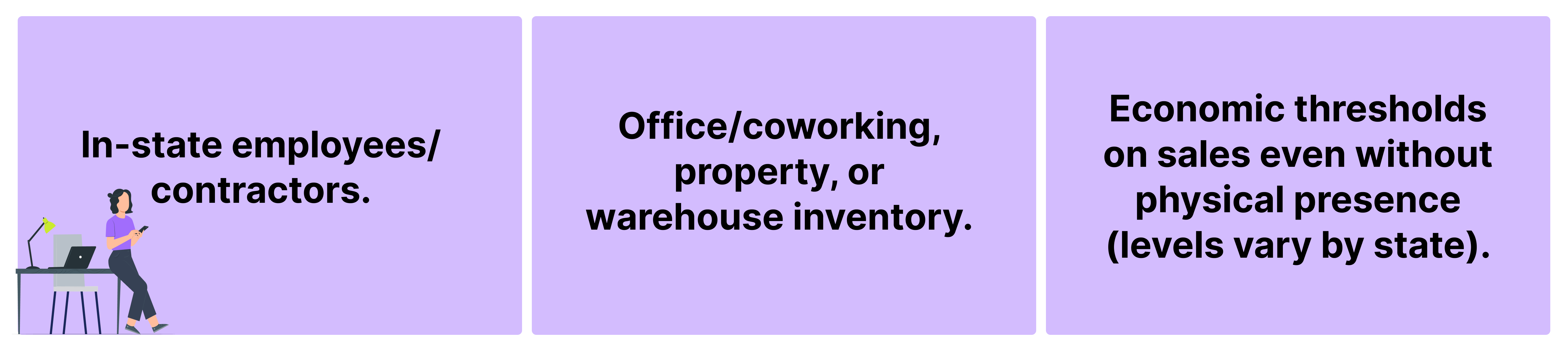

Presence (not intent) usually determines whether a state can tax you.

What creates a taxable presence

Remote-first pitfalls: One new hire in a state can create withholding, unemployment, and filing obligations; apportionment then allocates income. Build a hiring checklist that includes registrations and payroll setup.

Learn more in → Minimizing State Income Tax for Remote-First U.S. Startups.

Pure SaaS is often non-taxable in certain jurisdictions (e.g., California), but taxable in others like New York or Texas. Downloadable software, physical media, or bundled hardware can also create taxable components. Define your product, split pricing on bundles, and automate rules (SKU matrix + rate updates).

Claiming R&D credits early can reduce payroll burn and extend runway. Eligible companies may use the federal credit to offset employer payroll taxes when income tax is low.

Substantiate with short project briefs, time records, and invoices. See more → Claim R&D Tax Credits as a Tech Startup.

QSBS may exclude a substantial portion of federal capital gains if strict tests are met:

Some states do not fully conform, state gains may still be taxable. Preserve minutes, ledgers, grants, and valuations.

Keep a simple rolling calendar with federal anchors:

See our → tax deadlines guide.

Separate pre-opening costs from operating expenses. Depreciate tangible property; amortize organizational/start-up costs unless immediate deduction is elected where allowed. Document policies, approvals, and schedules so tax and GAAP stay aligned.

Delaware offers governance advantages; however, when a Delaware company operates in another state, it must register as a foreign entity, open state payroll accounts (if applicable), and file local tax returns. Expect dual obligations—Delaware franchise tax plus the franchise or income tax of the operating state. Register early, keep certificates of authority, and track renewal dates to maintain compliance.

Close books monthly, reconcile key accounts, and maintain a chart of accounts that separates R&D, capitalization, and operating expenses. Set up payroll accounts before the first hire, classify workers correctly, and schedule estimates to avoid underpayment penalties.

Simple checklists for payroll, information returns, nexus, and R&D documentation turn compliance into routine.

We turn complex compliance into predictable operations:

We align tax strategy with fundraising and equity plans so attributes survive diligence. Meet our team or schedule a free consultation.

A compliance-first approach makes taxes repeatable and defensible. Keep a living calendar, tight documentation, and monthly closes; preserve NOLs, capture R&D credits early, treat remote hires as state events, and plan QSBS with counsel. We’re ready to help operationalize this roadmap so you can scale with confidence.

• Federal: get an EIN, file the right return (corporate/partnership/individual with business schedule), and pay federal income/payroll taxes.

• State: varies by nexus, may include income/franchise/gross-receipts tax, sales & use tax, and employer withholding with state-specific thresholds and deadlines.

• Match the entity: C-Corp → corporate return; Partnership/multi-member LLC → partnership return; Sole prop → individual with business schedule; S-Corp → corporate return after election. Weigh investor needs, payroll, and exit plans.

When raising VC, issuing options, and scaling fast. Pros: equity tools, potential QSBS. Cons: corporate-level taxation. Choose if benefits outweigh costs.

• LLC: flexible pass-through; owners may owe self-employment tax.

• S-Corp: can reduce self-employment via reasonable compensation; has shareholder/class restrictions.

Physical presence (employees, office, inventory) or economic presence (sales thresholds/transactions). Remote hires and marketplaces can trigger registrations and filings.

It’s state-specific. Pure SaaS can be non-taxable in some states, but downloads, media, or bundled hardware may be taxable. Classify each SKU correctly.

If sales tax wasn’t collected, use tax may apply. For bundles, allocate price between taxable and non-taxable components and document contracts/invoices.

Tech-driven work with uncertainty and experimentation. Eligible costs often include wages, supplies, and contract research. Substantiate with project briefs, time tracking, and cost allocations.

Yes, when eligible. Coordinate with payroll to apply credits correctly.

They generally carry forward with annual usage limits; state rules vary. Track NOLs by year and jurisdiction.

Potential federal gain exclusion if you meet statutory requirements and a multi-year holding period. Some states don’t conform, plan state tax separately.